Heavyweights dominate the Swiss stock market

In the last Research Insights article «The low-volatility anomaly put to the test», we looked at the low-volatility anomaly in Switzerland and found that the excess return of this factor strategy has not diminished in recent years. Nevertheless, some defensive strategies in the Swiss equity market have recently failed to beat the SPI benchmark - despite the general market weakness. We are on the trail of the reasons.

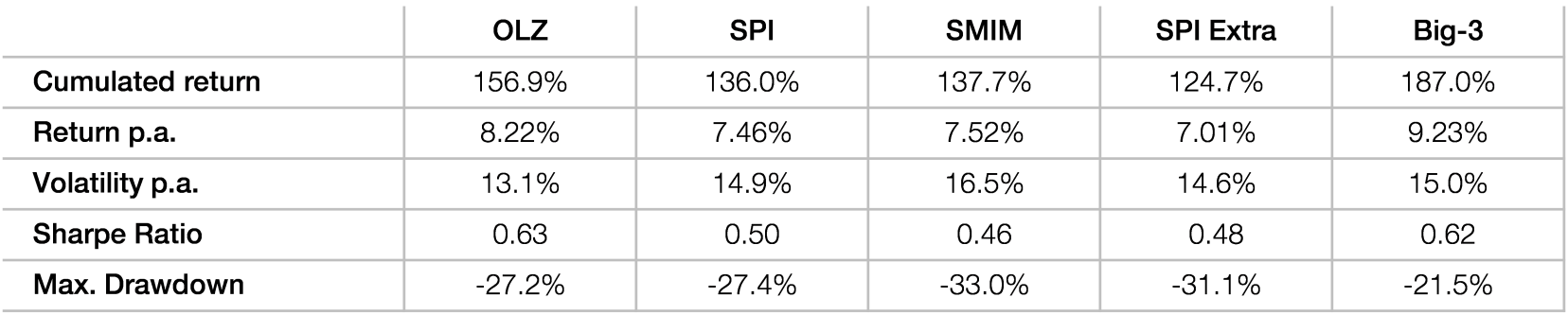

When thinking of Swiss stocks, Nestlé immediately comes to mind for many investors. With a market capitalization of more than CHF 300 billion, the world's largest food company is also a heavyweight on the international stock markets, making it into the world's 20 largest listed companies. But the numbers two and three on the Swiss stock market are not much smaller: Roche has a market capitalization of around CHF 240 billion, while Novartis has a market capitalization of around CHF 190 billion. Taken together, these three heavyweights, named «Big-3» for short, have a total capitalization of just under 50% of the SPI Index (see Figure 1). In addition, two of these stocks, Roche and Novartis, come from the pharmaceutical sector. This historically high concentration of Big-3 stocks in the SPI makes the index top-heavy and entails a significant cluster risk that many investors are unwilling or unable to take for regulatory reasons.