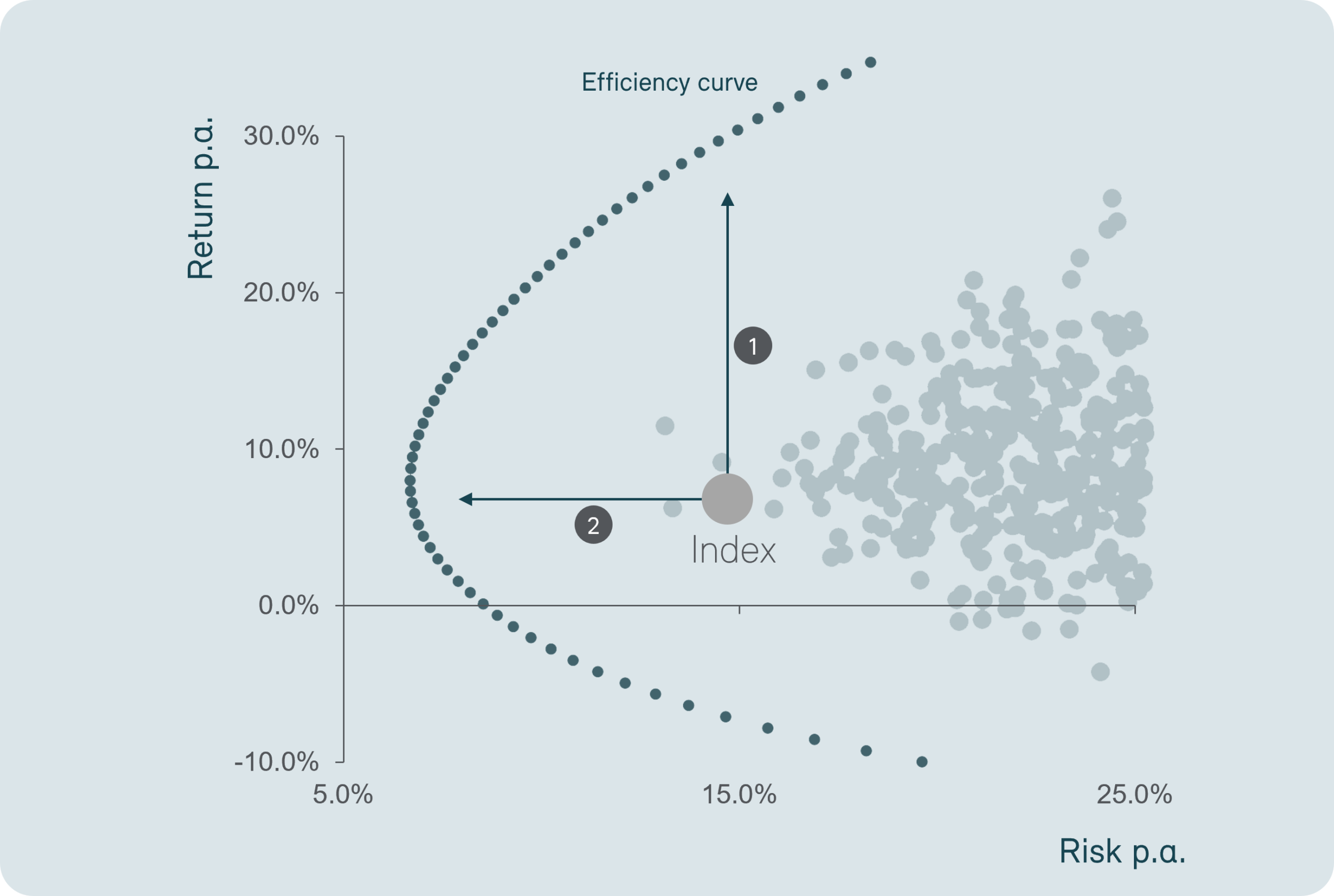

Standard indices are not efficiently composed

Standard indices weight stocks according to size. This means that the larger a company's market capitalization, the greater its weight in the index. Financial market research confirms that this composition is far from optimal. From a risk/return perspective, a portfolio can be constructed more efficiently in order to subsequently lie on the efficiency curve.

Through our optimization to an efficient portfolio

In order to construct an efficient portfolio and thus be on the efficiency curve, return forecasts are required for all eligible securities. One exception is the so-called “ex-ante minimum variance portfolio,” the portfolio with the lowest risk. For this portfolio, risk forecasts that can be made more reliably and with less uncertainty are sufficient. This is exactly where our minimum variance approach comes in. We forecast the risk characteristics for each individual stock within a stock universe and use this to derive an optimally composed portfolio that also takes into account the correlations between the stocks. The portfolio is not only risk-optimized and diversified, but also takes strict sustainability criteria into account.