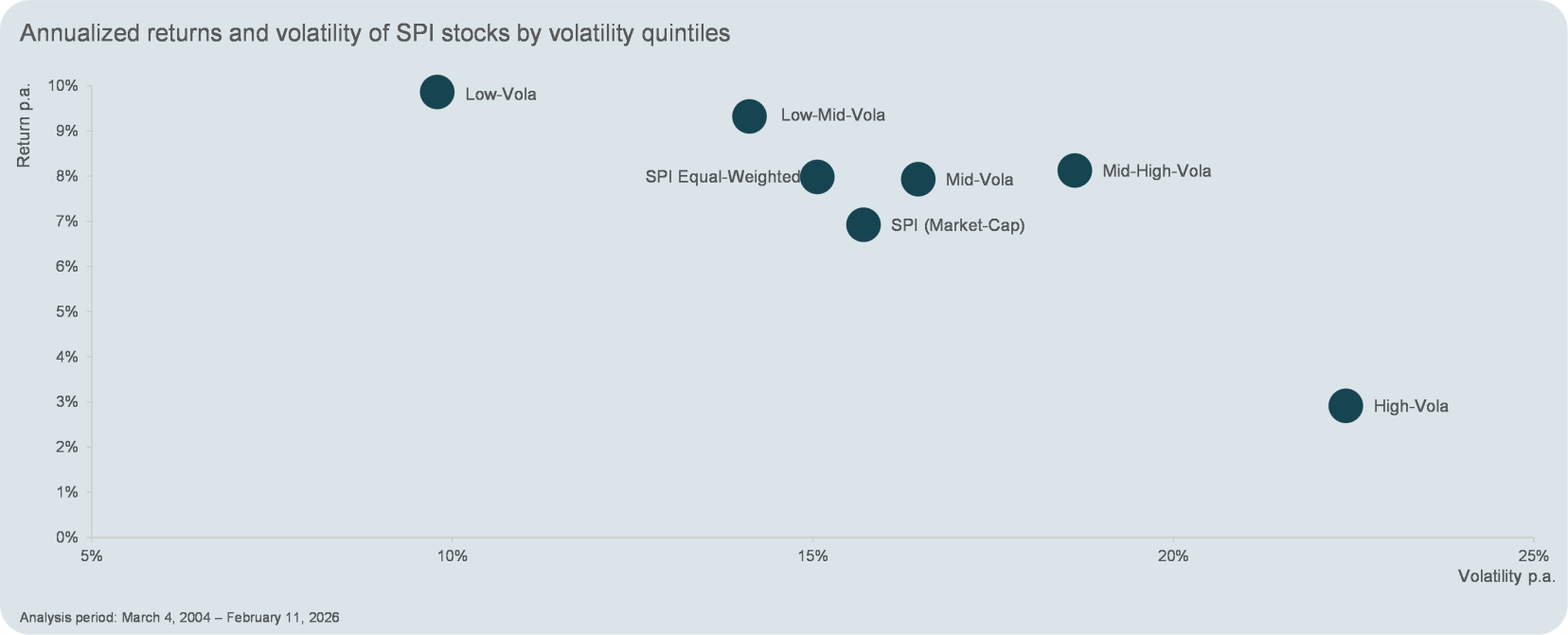

The minimum-variance approach aims to combine securities in such a way that the overall risk of the portfolio is minimized as much as possible. What is relevant here is the covariance structure of the entire universe—not a one-dimensional ranking based on volatility. To achieve the highest possible quality in the estimation of the covariance matrix, the OLZ minimum variance models therefore use a state-of-the-art estimator—the so-called Quadratic Inverse Shrinkage (QIS) estimator. This significantly reduces estimation errors in the risk parameters, leading to a more efficient and robust minimum-variance portfolio. In addition, liquidity filters, position restrictions, and turnover controls play a crucial role as part of regular portfolio rebalancing.

OLZ Minimum Variance Strategy with a Strong 15-Year Track Record

Although there have been cautious model updates over time to consistently incorporate new scientific findings, OLZ AG has been following this approach in the OLZ Equity Switzerland Optimized ESG Fund for over 15 years. The table below shows that since its inception, the fund has not only achieved an attractive return after costs but has also been able to reduce risk. Today, the OLZ fund is the largest publicly offered fund with a minimum variance focus for Swiss equities.

| OLZ Equity Switzerland Optimized ESG | Swiss Performance Index (SPI) |

Period | Cumulative Return | Volatility p.a. | Sharpe Ratio | Max. loss | Cumulative return | Annual volatility | Sharpe ratio | Max. loss |

YTD | 4.4% | 9.7% | 2.5 | -3.9% | -0.5% | 12.1% | -0.2 | -6.7% |

1 year | 9.3% | 10.3% | 0.9 | -9.3% | 5.1% | 13.8% | 0.4 | -15.7% |

3 years | 28.8% | 9.1% | 0.9 | -9.3% | 27.5% | 11.7% | 0.7 | -15.9% |

Since inception | 230.4% | 12.4% | 0.6 | -27.3% | 209.2 | 14.2% | 0.5 | -27.4% |

As of March 10, 2026; OLZ Equity Switzerland Optimized ESG launched on December 20, 2010. Note: Past performance is not a reliable indicator of future results. |

Another market segment where a risk-optimized investment strategy can be particularly rewarding is small- and mid-caps. In the Swiss stock market, the SPI Extra represents this investment universe. Historically, companies with small and medium market capitalization have generated higher returns than large caps—an effect known as the size premium. However, academic studies have shown that this excess return can be significantly increased by filtering the riskiest small-cap stocks out of the investment universe. The OLZ Equity Switzerland Small & Mid Cap Optimized ESG Fund pursues precisely this goal through minimum variance optimization of the SPI Extra universe. As the table below shows, the OLZ fund’s performance since launch has far outperformed the benchmark index, the SPI Extra. In the current Citywire ranking, the OLZ Equity Switzerland Small & Mid Cap Optimized ESG therefore ranks first over three years in terms of return, volatility, and maximum loss[1] .

| OLZ Equity Switzerland Small & Mid Cap Optimized ESG | SPI Extra |

Period | Cumulative Return | Volatility p.a. | Sharpe Ratio | Max. loss | Cumulative return | Annual volatility | Sharpe ratio | Max. loss |

YTD | 5.6% | 9.1% | 3.4 | -2.4% | 1.1% | 11.8% | 0.5 | -5.0% |

1 year | 18.1% | 9.2% | 1.9 | -7.4% | 11.2% | 12.9% | 0.8 | -13.6% |

3 years | 40.3% | 8.7% | 1.3 | -8.2% | 20.2% | 11.6% | 0.5 | -15.2% |

Since inception | 45.7% | 8.7% | 1.4 | -8.2% | 27.3% | 11.8% | 0.6 | -15.2% |

As of March 10, 2026; OLZ Equity Switzerland Small & Mid Cap Optimized ESG launched on December 15, 2022. Note: Past performance is not a reliable indicator of future results |

Conclusion: Minimum-variance portfolios deliver attractive equity returns with less risk

The minimum-variance approach offers a systematic way to reduce volatility and drawdowns within the SPI or SPI Extra universe without sacrificing the long-term equity market premium. While the approach cannot outperform in every phase—during strong rallies, a defensive portfolio will tend to lag behind the benchmark— However, over a full cycle, the goal of providing Swiss equities with a more efficient risk profile and a more stable return path is achievable—the OLZ funds prove this! For investors who take not only the return but also the path to it seriously, this approach is highly relevant in a world marked by uncertainty.

[1] See: https://citywire.com/ch/sector/equities-switzerland-small-and-medium-companies/i1569?periodMonths=36, website accessed on March 10, 2026