ESG is particularly important in the small- and mid-cap segment. Many small and mid-sized companies attract less attention from analysts and the public than large blue-chip firms. Consequently, differences in governance structures, transparency, and issuance profiles are often more pronounced. This presents investors with the opportunity to measurably improve a portfolio’s sustainability quality through targeted selection.

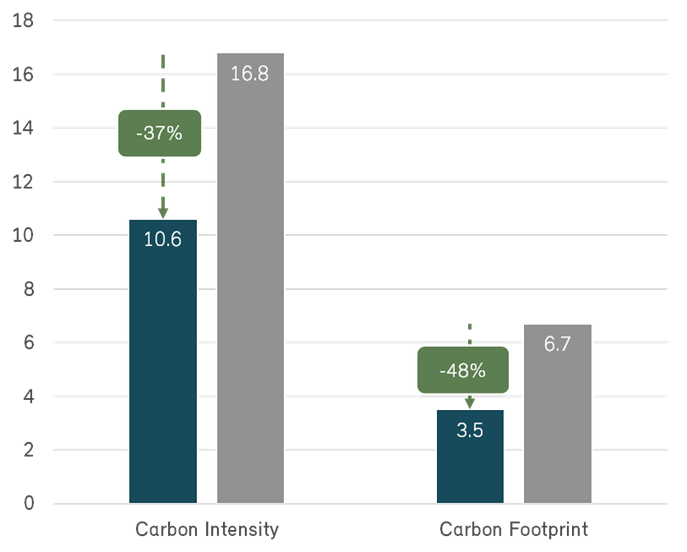

One example of such an approach is the OLZ Equity Switzerland Small & Mid Caps, which invests in the SPI Extra universe and systematically integrates ESG into the investment process. The impact of this approach is evident in both ESG ratings and concrete climate metrics.

Making ESG measurable: MSCI ratings and CO₂ metrics

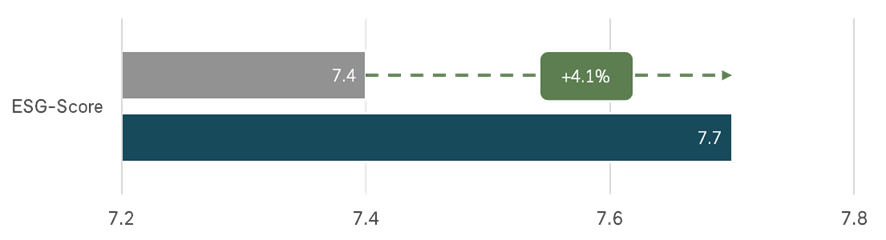

A key benchmark is the MSCI ESG Score, which assesses how well companies manage material environmental, social, and governance risks. The assessment is industry-specific, allowing companies to be compared within their respective sectors. The score is based on exposure to ESG risks as well as the quality of risk management.

Compared to the SPI Extra, the OLZ portfolio has a higher average ESG score (7.7 versus 7.4). This suggests that, on average, the companies included in the fund are better positioned to address ESG-related issues than the overall market.