High valuations reduce expected returns

In the context of these high valuations, the question arises as to whether prices can continue to rise and move further away from their fundamental valuation. Naturally, high valuations reduce expected returns.

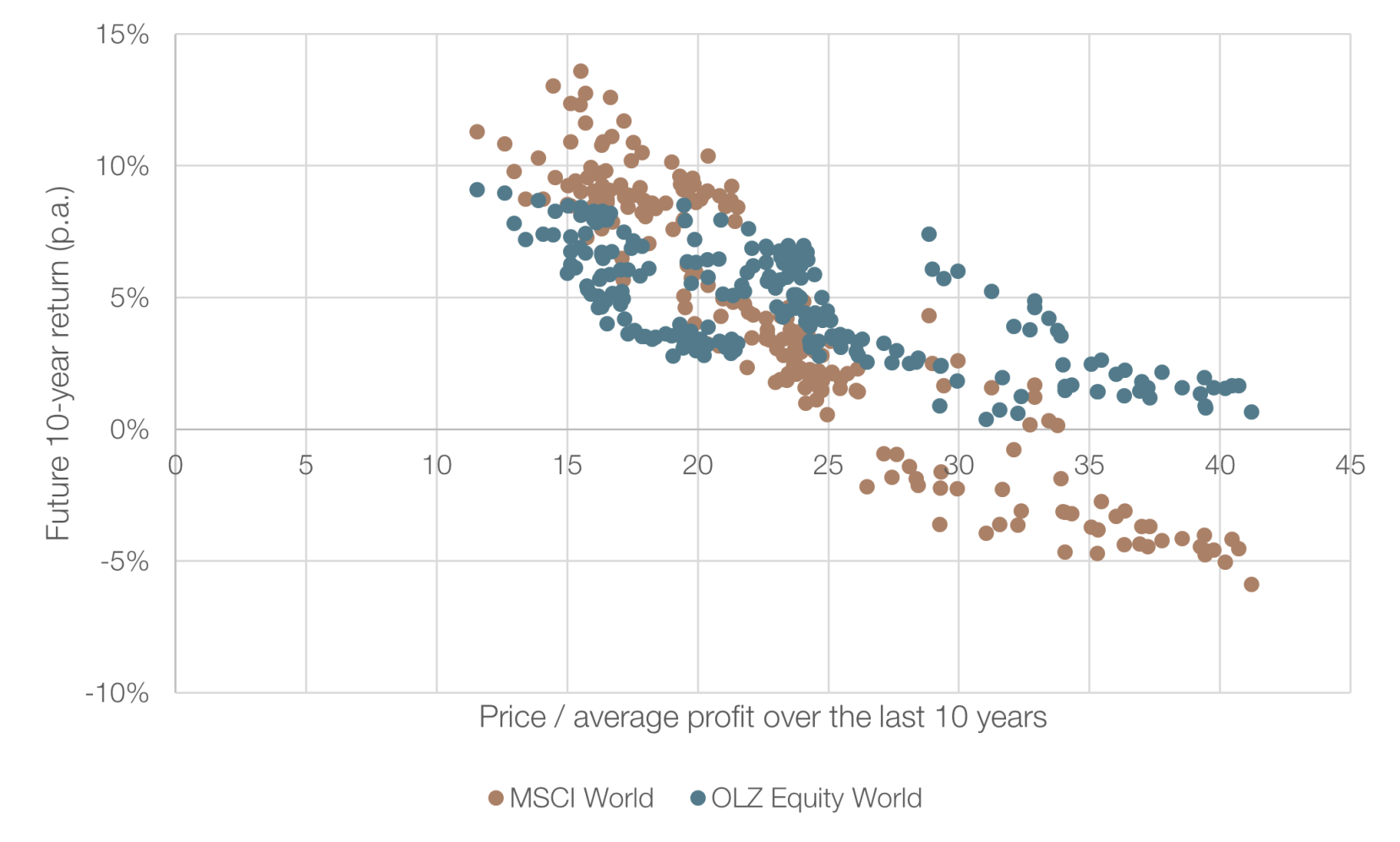

This correlation has been empirically proven in a large number of academic publications. One of the best-known papers on this subject was written by Campbell and Shiller (1998)* and shows that the relationship between current valuations and future 10-year returns is linearly declining.

In order to understand how OLZ risk optimization relates to the valuation of the MSCI World, we examined the valuation of the MSCI World in relation to the future 10-year return of the MSCI World and the risk-reduction-oriented OLZ Equity World Optimized Fund, using a methodology similar to that of Campbell and Shiller.

Our analysis confirms the negative correlation between the valuation of the MSCI World and the future expected return of the MSCI World. With regard to the performance of the OLZ fund, an interesting observation can also be made: regardless of the valuation of the MSCI World, the performance over 10 years is always positive. The annualized return over 10 years fluctuates between 0.4% and 11.2% for the risk-optimized OLZ fund, while the MSCI World returns between -5.9% and 13.6%. This makes it clear that, in the best-case scenario, investors earn around 2.4% p.a. more with the MSCI World than with the OLZ fund, but they can also lose an average of -5.9% per year over 10 years.