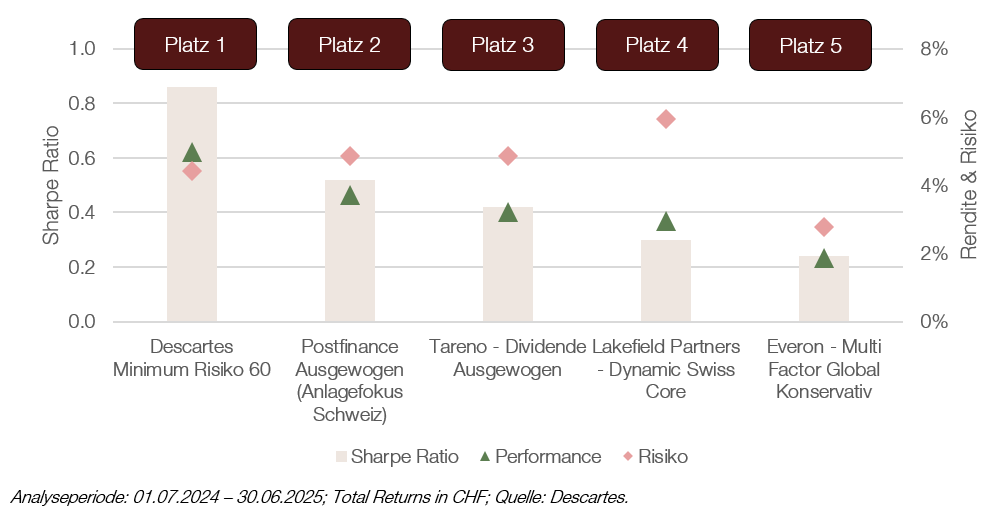

The Descartes Minimum Risk 60 strategy not only achieved the best risk-adjusted performance over the past 12 months, but also the best absolute performance, beating its competitors in the “Conservative” category.

OLZ Minimum Risk with top performance in balance sheet comparison

Our partner Descartes secures first place with our risk-optimized strategy. We are delighted to receive the Bilanz award for the best conservative investment strategy 2024/2025.

This award demonstrates that even with a moderate increase in uncertainty—as has been observed since the end of 2024—the risk-optimized strategy can create significant added value: While the MSCI World Index returned 1.95% over the period, risk (measured by 1-year volatility) more than doubled.

A look at history shows that such an increase in risk is by no means unusual and is rather moderate compared to the financial crisis of 2008 or the coronavirus crisis of 2020. In such phases, OLZ risk optimization can generally outperform significantly and massively reduce losses in negative markets. Disciplined investors who can accept underperformance in strong bull markets benefit from disproportionate outperformance in volatile market phases, which allows them to achieve excess returns over a passive benchmark in the long term.

What makes the balance sheet comparison so unique

A methodologically sound comparison of different investment strategies is based on the ratio of return to risk. While there is broad consensus on how to measure returns, assessing risk is much more complex. Most comparisons of different investment strategies base their risk assessment solely on the equity allocation. The problem with this approach is that it completely ignores the composition of the equity allocation and therefore does not take into account the actual measured risks, such as volatility or maximum loss in value.

Balance sheet comparison, on the other hand, categorizes the strategies to be compared on the basis of the measured risk. Each strategy is thus classified into one of four risk categories, so that the returns generated can then be analyzed for comparable risks.

The following chart illustrates the results of the two comparisons – one based on the equity allocation and one based on risk:

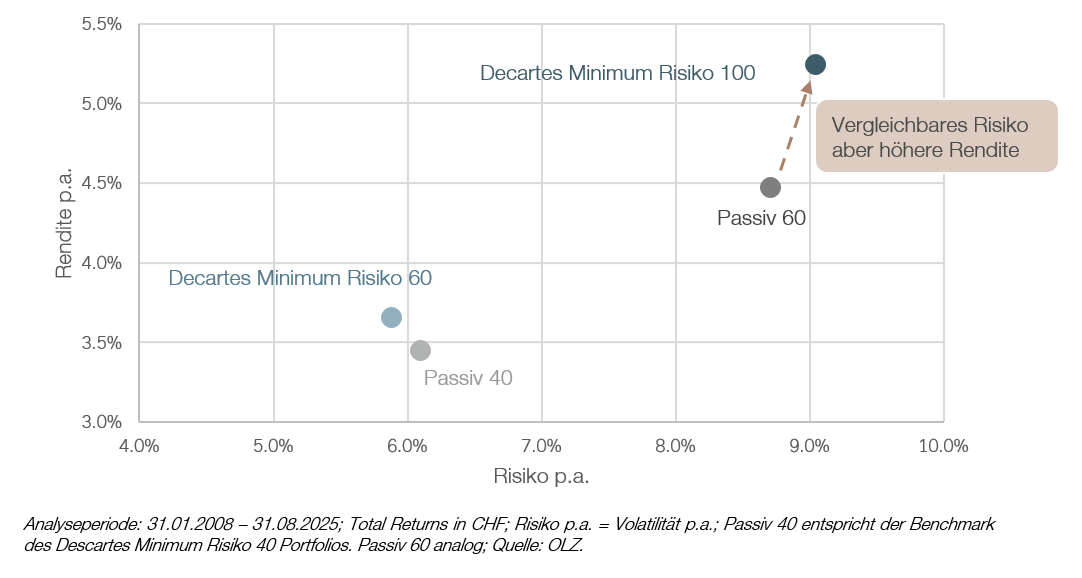

Those who only look at the equity allocation may mistakenly compare the Descartes Minimum Risk 60 portfolio directly with the Passive 60 portfolio. In terms of performance, the passive portfolio would come out on top: while the Passive 60 portfolio generates 4.5% per year, the Descartes portfolio achieves 3.7% p.a. However, a look at the risks shows that the passive portfolio has a volatility of 8.7% and a maximum loss in value of 29.1%. The Descartes portfolio, on the other hand, has significantly lower risks, with a volatility of 5.9% and a maximum loss in value of 16.2%.

Looking at the actual risks taken, the Descartes Minimum Risk 60 portfolio can be compared with the Passive 40 portfolio, which has a volatility of 6.1% p.a. and a maximum loss in value of 18.8%. The annual return of the Descartes portfolio, at 3.7%, is even slightly higher than the annualized performance of the Passive 40 portfolio, at 4.5%.

Following this logic, the Descartes Minimum Risk 100 portfolio is the fair benchmark for the Passive 60 portfolio due to its comparable risk profile. While the Descartes 100 portfolio has a volatility of 9.1% p.a. and a maximum loss of 28.3%, its performance of 5.2% exceeds the return of the Passive 60 portfolio. This clearly shows that risk reduction increases disproportionately with the equity allocation, so that a risk-optimized 100% equity allocation is comparable to a passive 60% equity allocation.

Conclusion: Those who compare investment strategies solely on the basis of equity allocation ignore the actual risks – and thus leave return potential untapped.